Key points

Baseline

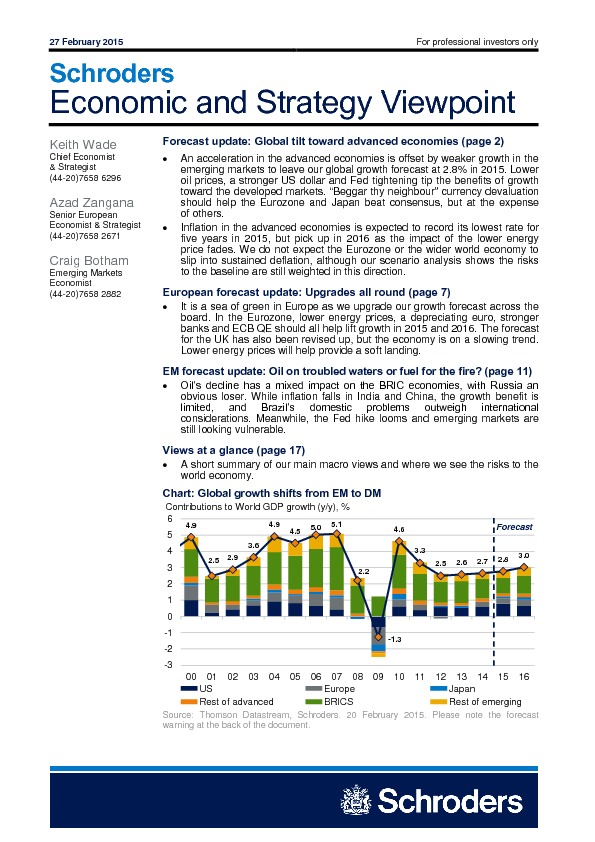

- Global recovery to continue at modest pace as the upswing in the advanced economies is offset by slower growth in the emerging markets. Lower energy prices will push inflation in the advanced economies to its lowest level since 2009.

- US economy on a self sustaining path with unemployment set to fall below the non-accelerating rate of unemployment (NAIRU) in 2015, prompting Fed tightening. First rate rise expected in June 2015 with rates rising to 1.25% by year end. Policy rates to peak at 2.5% in 2016.

- UK recovery to moderate in 2015 with cooling housing market, political uncertainty and resumption of austerity. Interest rate normalisation to begin with first rate rise in November after the trough in CPI inflation. BoE to move cautiously with rates at 1.5% by end 2016 and peaking at around 2.5% in 2017.

- Eurozone recovery firms as fiscal austerity and credit conditions ease whilst lower euro and energy prices support activity. Inflation to remain close to zero throughout 2015, but to turn positive again in 2016. ECB to keep rates on hold and continue sovereign QE through to September 2016.

- Japanese growth supported by weaker yen, lower oil prices and absence of fiscal tightening in 2015. Momentum to be maintained in 2016 as labour market continues to tighten, but Abenomics faces considerable challenge over the medium-term to balance recovery with fiscal consolidation.

- US still leading the cycle, but Japan and Europe begin to close the gap in 2015. Dollar to remain firm as the fed tightens, but to appreciate less as ECB and BoJ policy is now largely priced in.

- Emerging economies benefit from advanced economy upswing, but tighter US monetary policy, a firm dollar and weak commodity prices weigh on growth. China growth shifting downward as the property market cools and business capex is held back by overcapacity. Further easing from the PBoC to follow.

Risks

- Risks still skewed towards deflation on fears of Eurozone deflationary spiral, China hard landing and secular stagnation. Upside growth risks on a return of animal spirits and a G7 boom, fiscal stimulus in the Eurozone and lower energy prices. Stagflationary risks centre around a further deterioration in the Russia/ Ukraine crisis culminating in a cut off in energy supply to Western Europe

Continue reading this article?

Register for free and get access to Investment Officer International:

- Exclusive for professional investors

- Cancel anytime

- Unlimited access: web, app and newsletters

Registration takes less than 1 minute.

No payment details required

Register for free and get access to Investment Officer Luxembourg:

- Exclusive for professional investors

- Cancel anytime

- Unlimited access: web, app and newsletters

Registration takes less than 1 minute.

No payment details required