China’s recent experiences of economic recovery and relative asset price performance provide useful insights into how the path for other countries and global markets may unfold, writes Evan Brown, Head Macro Research at UBS Asset Management in his latest Macro Monthly.

Right now, investors are working from a common set of assumptions: Global activity is poised to meaningfully accelerate as vaccinations allow for a durable economic reopening. According to Brown, this conventional wisdom does not make asset allocation any easier. “To the contrary, the extent to which these consensus opinions are embedded in market prices may make deciding where and how to take risk a more difficult endeavor. Identifying leading indicators that may shed light on how activity and asset prices will unfold is an essential tool for investors.”

Lesson 1: Stay in early cycle regions

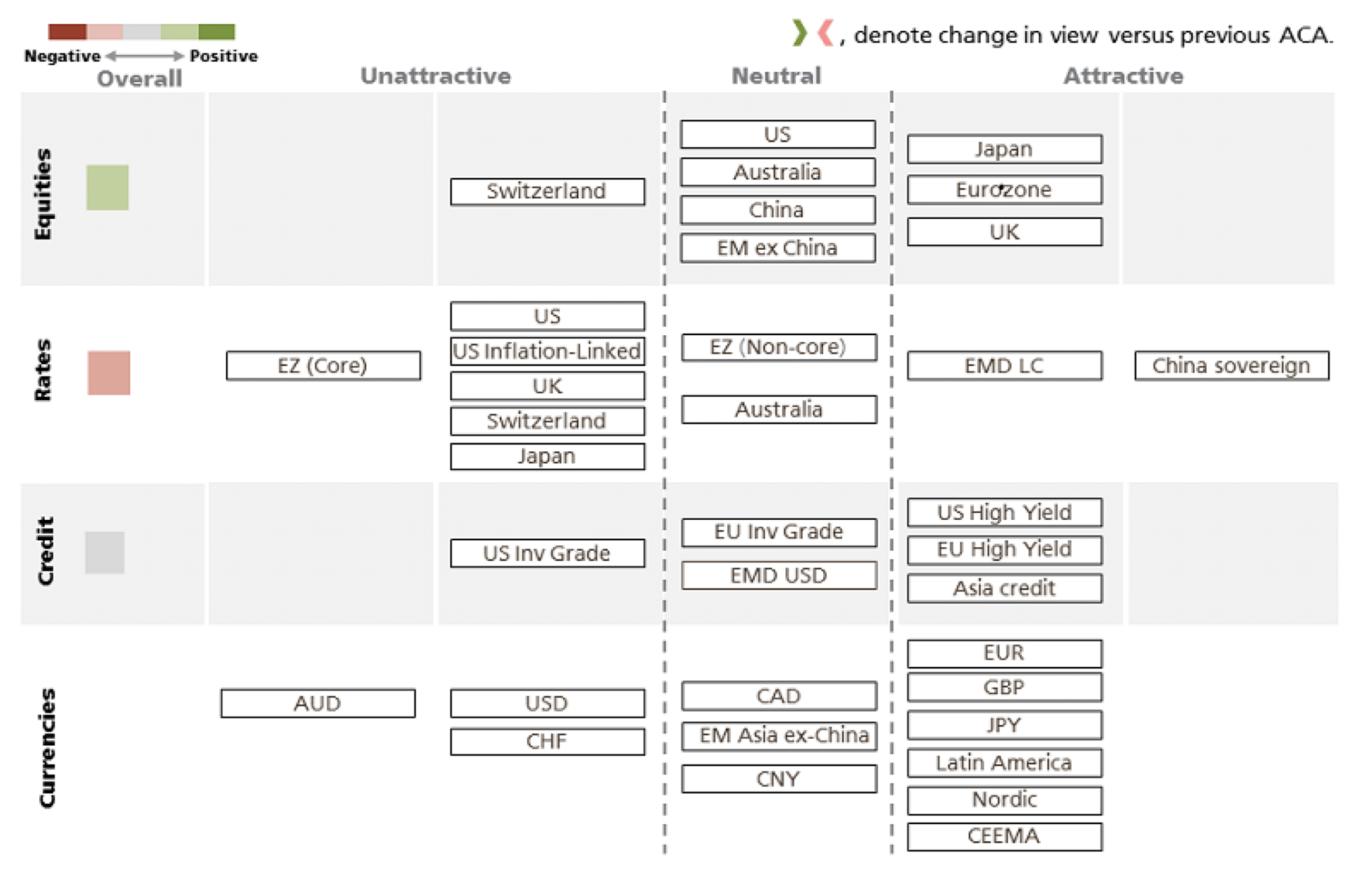

“But throughout 2021, Chinese activity will likely be decelerating. This relative lack of momentum is reflected in the divergence in earnings revisions between Chinese and global equities. Calendar year 2021 earnings per share estimates for the MSCI All Country World Index have been upgraded by 10% since the start of the year. Meanwhile, profit forecasts for the MSCI China Index have been trimmed by nearly 3%. That has contributed to Chinese equities underperforming all other major regions year to date, a reversal of last year’s leadership. This experience for Chinese equities may be a prologue to what awaits their American counterparts and bolsters our conviction to stay in early-cycle geographies. Ex-US stocks over US stocks.

Lesson 2: Don’t fade the factory boom too soon

“Manufacturing output and exports remain resilient in China, a reminder that investors should focus risk exposures in markets levered to the continued strength in goods. But momentum in goods goes far beyond China. The flash readings of manufacturing purchasing’ managers indexes posted fresh cycle highs in the eurozone, US, UK, Australia, and Japan – which all are indicating faster rates of growth in factory activity than China. Vaccinations that enable a rebound in services sector activity will be adding another pillar to the global growth outlook, which is slated to stay well-buttressed by solid manufacturing production.”

Lesson 3: Policy will likely be less stimulative, but nowhere near tight

“The chief risk to procyclical positions is if policymakers prematurely withdraw stimulus and jeopardize the recovery. However, Beijing has pledged to avoid an abrupt turn in policy from stimulus to tightening and outlined a course of action aligned with this commitment. Central banks in advanced economies are remaining patient, largely signaling a continuation of extraordinary accommodation even as activity improves. This enduring commitment from policymakers – on both the monetary and fiscal side, in China as well as the rest of the world – to act as stewards of the expansion supports risk assets relative to developed market sovereign bonds as well as our procyclical relative value trade set.”

Lesson 4: Policy risks are two-sided

“The risk: China also shows us that policy risks will become more two-sided as economies fully heal. That being said, the extent of the economic recovery means that policymakers in China no longer need to have a single-minded focus on supporting activity. Their policy agenda reveals that, as well: Modest fiscal consolidation is still consolidation. Since the global financial crisis, pullbacks in Chinese credit growth have coincided with an contributed to softness in global goods activity and weakness in equites, with long and variable lags. But these lags have been getting shorter as market participants have a thorough understanding of China’s importance to the global industrial cycle.”

Conclusion:

“As more and more economies experience the same degree of economic healing as China, the challenges facing asset allocators will increase. But so too will this evolution enhance the appeal of globally-diversified multi-asset portfolios that allow investors to be nimble in adapting to changes in the macroeconomic environment.”

Here you'll find the complete Macro Monthly ‘Four investing lessons from China’s recovery’ from UBS Asset Management.