A year on from the world entering lockdown and stock markets plummeting, vaccine rollouts and economic reawakening signal optimism for a sustained revival.

From an investor perspective, March 2020 marked the nadir of the Covid-19 pandemic. Global stock markets lost 12% of their value and volatility hit record levels as the world was forced into shutdown[1]. Much has happened in the twelve months since those dark days of uncertainty and global equities thankfully recovered in record time to reach new highs by the end of 2020, helped by unprecedented economic stimulus. Even more positive and remarkable is that success in the discovery and rollout of vaccines means that the end of the tunnel now appears within sight.

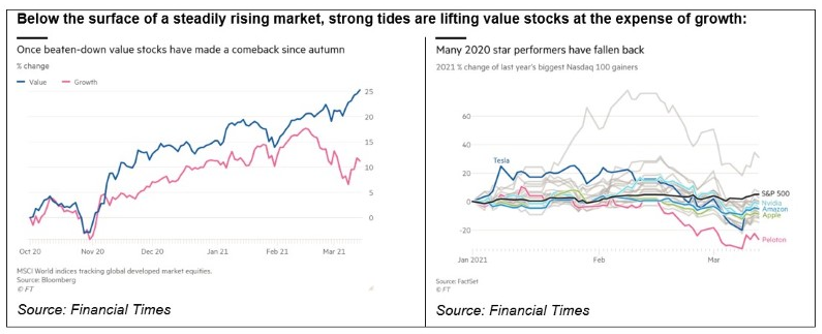

I am also happy to report that since my previous update, the anticipated value recovery continues to gather pace. Investors' optimism for a stronger global economy has been the driving force behind value's resurgence. Unemployment is down while incomes and consumer spending are up as people grow increasingly confident about the post-pandemic future. This means inflation is expected to rise, pushing up long-term interest rates (the 10-year US government bond yield has climbed to 1.6% from 0.7% a year ago) and thereby reducing the present value of future earnings for popular growth stocks.

The global value benchmark is up 4.5% since march and 9.1% higher than the beginning of February[2], while the value-centric Dow Jones Industrial Average last week reached the highest point in its 125-year history[3]. At the same time growth stocks have tumbled and the tech-heavy NASDAQ 100 index last week entered correction territory after dropping more than 10% from its own record high.

Below the surface of a steadily rising market, strong tides are lifting value stocks at the expense of growth:

Rotation momentum

While the market dynamics between growth and value are currently undergoing a major shift, the question remains how sustainable will it be? This is impossible to answer – and there have been several false dawns during value's decade of underperformance – but there is growing evidence that its strong rally could become a longer-term recovery.

The IMF recently upgraded its growth forecasts for the global economy and now expects GDP to expand 5.5% this year and 4.2% in 2022[4]. This confidence is shared by investors with stocks in sectors which are sensitive to the economic cycle such as banking, energy, materials, commodities, consumer goods and industrials in particularly high demand. The most optimistic believe that the Covid recovery could mirror the 'roaring 20s', a decade of post-war hedonism characterised by deferred consumer spending and infrastructure investment.

While vaccine rollouts are helping to reawaken the global economy from hibernation, government stimulus is also providing a shot in the arm for value stocks, notably in the US where President Biden’s $1.9tn programme was enacted. A recent Deutsche Bank survey of 430 private investors found that on average they plan to invest over a third of their direct $1,400 payments in the stock market and data from Morningstar Direct shows that US value funds attracted double the amount of capital in February as growth ones[5]. January also saw net inflows after sustained outflows during the pandemic and value stocks should receive further support if the trend continues.

Stockpicker's market

A knock-on effect of growth companies faltering is that the FAANGM share of the S&P500 Index weighting has fallen from around 27% to 23% over the last four months[6]. Although still high, the market is becoming less distorted which is good news for stockpickers. The correlation between stocks has fallen to below-average levels this year meaning that there is greater differentiation between them. More significant for highly active managers like SKAGEN is that dispersion, or the difference between individual stock returns, is currently at levels not seen for a decade. This means that as well as more opportunities to beat the market, the potential gains from picking the right stocks are greater.

The flip side to a market offering increased rewards is higher risk. CNN's Fear & Greed Index of market sentiment is signalling growing levels of greed, in stark contrast to the extreme fear of a year ago as we entered the pandemic. Just as then would have been a great time to buy the market with global equities climbing 45% in the subsequent 12 months, now is probably a risky time to own it[7]. Bubbles have formed and it is much safer to hold cheap companies likely to deliver immediate earnings growth than expensive ones whose future profits are uncertain and dwindling in present value.

From a SKAGEN perspective, the majority of our equity funds are beating their benchmarks this year and all look well placed to deliver strong performance, thanks to the investment teams' hard work to steer the portfolios through the pandemic and ready them for the economic recovery we all hope comes next. One swallow may not make a summer, but if value continues to outperform over the coming months then it will be hard to argue that a sustained recovery is well underway when the seasons change again.

For more information you can contact

e-mail: michel.ommeganck@skagenfunds.com

Mobile: +4790598412

Or via: www.skagenfunds.lu

References

[1] MSCI All Country World Index in EUR [2] MSCI All Country World Index Value in EUR [3] Source MSCI, as at 11/03/2021 [4] Source: IMF. World Economic Outlook, January 2021 [5] Source: Morningstar Direct. US-domiciled open-ended and exchange traded net fund inflows: Value +$6.3bn; Growth +$3bn [6] Source: Yerdeni Research as at 12/03/21. FAANGM = Facebook, Apple, Amazon, Netflix, Google (Alphabet) and Microsoft [7] MSCI All Country World Index in EUR as at 12/03/21