While the COVID-19 pandemic has generally been painful for real estate markets, it also highlights the relative benefits of listed property assets and the importance of being selective.

Global real estate markets are experiencing their toughest year since the global financial crisis. Most international indices have fallen between 10-20% in 2020[1], reflecting the global spread of COVID-19 and the direct property impact from prolonged lockdowns and falling economic activity. As with the funds that invest in their assets, however, not all property was created equally, and the headline figures mask differences between sectors, which can best (or sometimes only) be exploited via public markets.

A major advantage of investing in listed property assets is liquidity. This benefits clients, who can buy and sell units easily, as well as the manager. As the COVID-19 crisis began to unfold, we were able to exit or reduce SKAGEN m2's riskier holdings and redeploy the proceeds in companies with more attractive characteristics. This wouldn't have been possible with private real estate assets (as investors who remain trapped in several funds subject to high-profile suspensions know to their cost).

New economy opportunities

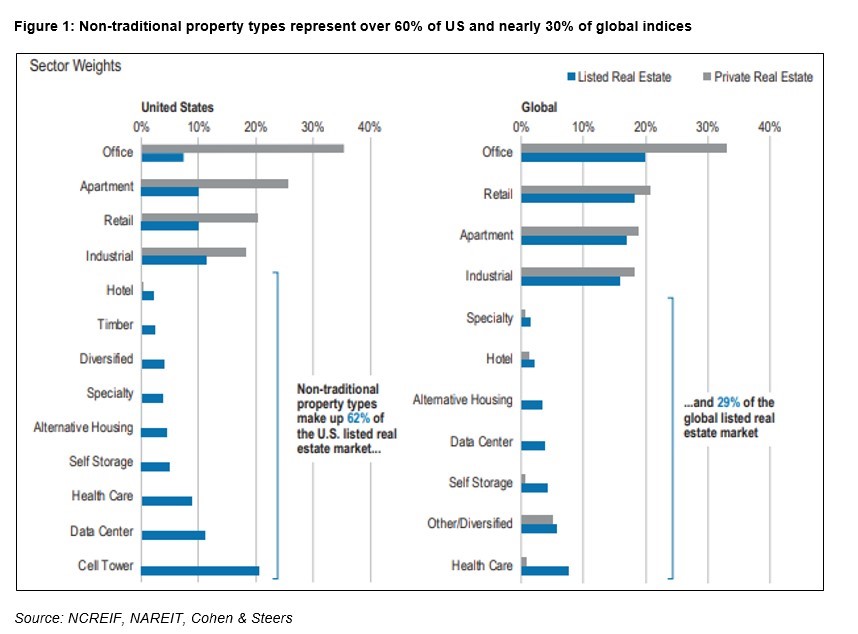

Public markets provide greater access to non-traditional real estate (see figure 1). These property assets are facilitating major structural trends which offer protection against cyclical downturns and are often impossible or difficult to access privately. The largest example in the US market is cell towers, which should benefit from secular growth as wireless carriers race to roll out 5G networks.

From a global perspective, health care is the largest non-traditional sector and illustrates a segment undergoing structural expansion as a result of changing demographics and an ageing population. We recently added Assura to the SKAGEN m2 portfolio, a UK REIT specialising in medical premises which owns over 570 GP surgery, primary care, diagnostic and treatment centres. The company has outperformed the broader real estate market and contributed positively to the fund, where it now represents 3.4% of assets. Helped by resilient rent collection and a strong NHS relationship, we believe it is well-positioned to capture the growing UK demand for healthcare premises, particularly post-Brexit.

Performance dispersion

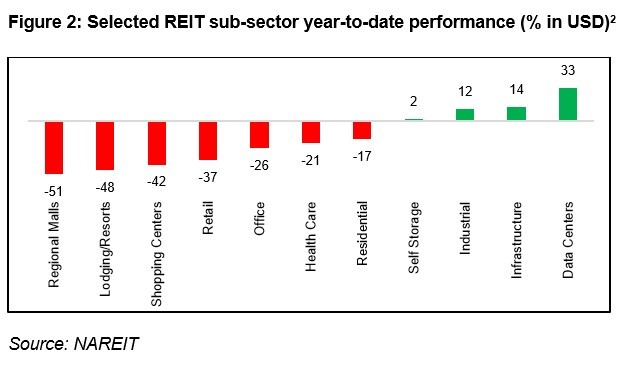

The wide-ranging effects of COVID-19 on real estate sectors will probably be felt for some time to come. This is also clearly reflected in varying equity performance as regional malls, lodging / resorts and shopping centres have suffered from continued restrictions and consumer anxiety while data centres and infrastructure (fibre cables, wireless infrastructure and telecom towers) have benefitted from remote working. The best and worst performing sectors in the US REIT market are typically separated by 40–60% over a calendar year whereas already in 2020 sector dispersion is over 80% (see figure 2).

SKAGEN m2's second largest holding (5.6% weight) and top contributor[3] in 2020 is US data centre provider, Equinix, whose share price has risen 35% in 2020. We recently added compatriot Switch (3.0% weight) to the portfolio, which is one of the purest plays to capture the proliferation of cloud technology. The company uses renewable energy to offer high reliability and delivered strong Q2 results with a 70% dividend increase while still expanding IT infrastructure to serve its growing market.

Research[4] shows that REITs outperform private real estate during economic recessions (-9.6% vs. -11.5% p.a.) and particularly during recoveries (+22.7% vs +2.8% p.a.). As well as their relative cyclical benefits, the charts above highlight that REITs are often the only way to access the strongest performing sectors which should continue to benefit long-term from structural technological and demographic growth drivers.

Office opportunities

The wide dispersion in returns has also amplified valuation differences between real estate sectors. Falling share prices mean that those trading at discounts to net asset value before the COVID crisis are now even cheaper and while this reflects heightened risks facing segments like hotels and retail, some now look attractive from a long-term risk-reward perspective.

The office sub-sector, for example, has seen discounts widen to 26% from 4% pre-crisis, which has created value opportunities in the right companies. Earlier we invested in Equity Commonwealth (2.4% of assets), a US office operator with four properties and a substantial cash pile after selling down a huge number of assets at premium price. The REIT is focused on distressed assets and should be able to find investment opportunities ahead, particularly given its strong balance sheet and prudent approach. We also initiated a new position in Allied (0.5% of assets) at an attractive discount. The Canadian REIT specialises in developing and operating office space near central business districts at lower occupancy costs than traditional skyscrapers and owns three urban data centres in Toronto.

While there will inevitably be macroeconomic challenges ahead, the disruption of global real estate markets, either caused by COVID-19 or longer-term structural shifts underway before the crisis, will present opportunities. The key to navigating these successfully will remain selective investment in listed companies, which provide unparalleled flexibility, liquidity and scope for investors.

References:

[1] FTSE E/N DEV Europe, MSCI ACWI RE IMI, Bloomberg US REITS, MACI ACAP RE indices (all USD, 31/12/19 – 31/07/20) [2] Source: NAREIT, performance in USD 31/12/2019 – 31/08/2020 [3] Absolute contribution in NOK 31/12/2019 – 31/08/2020 [4] Source: The Conference Board, NBER, Morningstar, NCREIF, Cohen & Steers, annualised returns in USD 1991-2019

For more information on our listed real estate fund SKAGEN m2 you can contact Michel Ommeganck

e-mail: michel.ommeganck@skagenfunds.com

Mobile: +4790598412

Or via: www.skagenfunds.lu